It

turns out that even the well-off need help in a housing market as crazy

as the one in the San Francisco Bay area, and lenders are elbowing each

other in a rush to provide it. They’re courting …

Silicon Valley Elites Get Home Loans With No Money Down

It

turns out that even the well-off need help in a housing market as crazy

as the one in the San Francisco Bay area, and lenders are elbowing each

other in a rush to provide it.

They’re courting Silicon Valley

workers with tailored loans, guaranteed 24-hour approval and

financial-planning services. Social Finance Inc. has deals with Google

and other top technology companies that allow it to market to new hires.

First Republic Bank -- which gave Facebook Inc. billionaire Mark

Zuckerberg a 1.05 percent interest-rate mortgage -- has opened branches

in Facebook and Twitter Inc. headquarters. San Francisco Federal Credit

Union will finance 100 percent of houses costing up to $2 million.

Michael

Tannenbaum, senior vice president of SoFi’s mortgage group, calls it

“white-glove service.” Lenders often give special treatment to the

wealthy, of course, but the tech industry has created a particularly

ripe crop of clients who are rich or on their way. It’s a smart bet to

cater to a sector that’s created thousands of millionaires and dozens of

billionaires, says Glenn Kelman, chief executive officer of the

brokerage Redfin. The downside is that the most expensive U.S. housing

region is becoming “a no-fly zone for anyone outside technology,”

especially with so many people shut out altogether by tight credit

standards imposed after the 2008 real-estate crash.

What’s

going on “might be good for the borrower and good for the lender,” he

says, “but it’s not necessarily good for San Francisco.”

‘Substantial’ Incomes

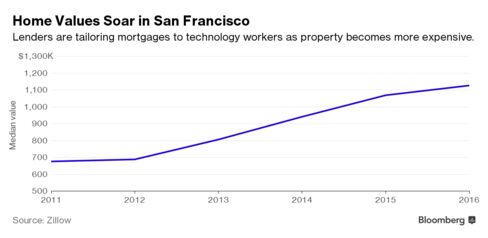

The

city’s median home value is $1.13 million, up almost 67 percent since

2011, and the numbers are higher in some nearby towns -- $6.36 million

in Atherton, according to Zillow Group Inc., and $4.12 million in

Hillsborough.

Nick Merz knows how tough it can be. He’s a

41-year-old product designer at Apple Inc. whose wife also works there,

and says they couldn’t figure out if they could afford to own a place

anywhere near the company’s offices in Cupertino, where the median value

is $1.8 million.

One reason: Almost half of their compensation

packages are in Apple shares. So their lender, Opes Advisors, assigned

the couple a financial adviser who used a software program to factor in

debts and future income, including the stock, and the costs of education

over the years for two young children.

‘Scary Market’

The

result? No problem. They could buy in the range they were looking

without jeopardizing their finances. “In a weird housing market, in a

place where a lot of assets are not liquid, it helps to have their kind

of modeling,” Merz says. “They’re catering to people scared by this

scary real estate market.”

For many, it’s not home values that

keep them in rentals but alarming down payments, which can be more than

the cost of the average U.S. house: $187,000. That’s where San Francisco

Federal Credit Union comes in. It started offering zero-down loans in

December to people who work in San Francisco or San Mateo County. The

credit union has more than $100 million pre-approved for 30-year

adjustable-rate mortgages in what’s called the Proud Ownership Purchase

Program for You.

As the tech boom starts to show signs of cracks,

there’s some concern that high loan-to-value mortgages are dangerous.

Silicon Valley venture-capital funding fell 20 percent in the second

quarter from a year earlier, according to a report

by PricewaterhouseCoopers and the National Venture Capital

Association. New companies are staying private longer, leaving fewer

options for shareholders to cash out.

The

median San Francisco condo price rose less than 1 percent in the second

quarter after an 18 percent increase a year earlier, data from Paragon

Real Estate Group show. Inventories of condos listed at $2 million or

more jumped 44 percent -- but the number sold fell 30 percent.

“Lenders

get so caught up trying to stay competitive and finding a market edge,

they basically allow greed to overcome common sense,” says Terry

Wakefield, a mortgage consultant who co-founded one of the first online

direct lenders in 1998. “Easy money does fuel and accelerate the

inevitable bubble.”

And the notion of 100-percent financing makes

some in the industry nervous. “Given what we went through in 2008,

zero-down financing is suicidal for our country,” says Chuck Green, CEO

of Bay Area Captial Funding Inc., a mortgage brokerage that offers loans

from about 40 different companies. “We have to learn from our

mistakes.”

‘Clients For Life’

For

its part, San Francisco Federal Credit Union sees the gamble as

manageable. Four in 10 applicants are rejected and those that have

gotten loans have an average FICO score of 747 and average household

income of $219,000, says Rebecca Reynolds Lytle, chief lending officer.

“We are vetting our borrowers to make sure they can afford it and have

reserves.” But in the end “it’s a loan -- it’s not going to be risk

free.”At Social Finance, the strategy is about getting in on the

ground floor, which it aims to do through its marketing partnerships

with 22 companies and a promise of an answer on a loan application

within a day to help speed up the home-buying process. SoFi also woos

clients with loan officers who fight to help them win bidding wars

against cash buyers.

Wells Fargo & Co., the largest retail

jumbo mortgage lender in the U.S., has been focusing on borrowers in

tech-heavy markets including San Francisco, Boulder, Colorado, and

Austin, Texas, says Brad Blackwell, the bank’s portfolio business

manager. Customers can qualify based on compensation tied to restricted

stock as long as they show that has been a stable source of income.

Lenders

are “targeting a segment that is the highest potential segment in the

country,” says Patrick Carlisle, chief market analyst at Paragon. “They

want these people to be clients for life.”

Before it's here, it's on the Bloomberg Terminal.LEARN MORE

Share E-mail

Share E-mail

No comments:

Post a Comment