begin quote from:

https://www.nbcnews.com/business/economy/household-finances-voters-economic-outlook-rcna153159

Clarity? In this economy?

Jim LaPointe knows that how the economy feels “depends on your perspective.”

Four years after Covid-19 lockdowns kicked off a home fix-up frenzy, the central New Jersey contractor’s business remains through the roof. While Home Depot said earlier this month that customers are increasingly holding off on big projects, LaPointe is seeing the opposite. He’s been turning some clients away to avoid being “booked up a year in advance.”

“They’re going nuts with this,” he said of homeowners’ appetite for renovations.

It wasn’t long ago when a stock market smashing records and unemployment at decadeslong lows were huge advantages for an incumbent president. But today, with voters heading to the polls in little more than five months, it’s less clear what role the economy will play in an electorate that’s also fractured by immigration and abortion rights.

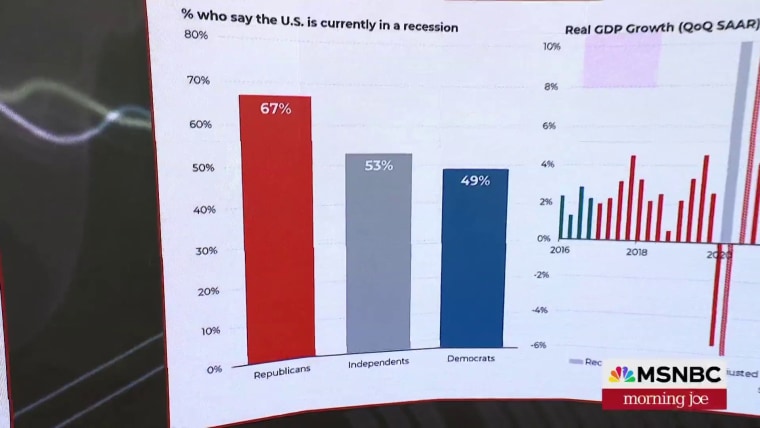

An NBC News poll last month found cost-of-living concerns remain top of mind for voters. While presumptive Republican nominee Donald Trump is seen — by a 52% to 30% margin — as better positioned to tackle inflation than his Democratic rival, President Joe Biden, 1 in 4 voters have yet to make up their minds about the race.

“We’re getting close to the period, usually in the summer, when public attitudes on the economy traditionally harden,” said Greg Valliere, chief U.S. policy strategist at AGF Investments, who so far sees Biden as “the clear underdog.”

The Biden campaign, which rejects that view, has been ramping up its economic messaging all year. It notes that the country dodged a much-forecast 2023 recession and weathered the Federal Reserve’s 11 interest rate hikes while continuing to add more jobs and small businesses.

The robust labor market and a Covid savings cushion mean many consumers continue to spend heavily, even those who face budget squeezes elsewhere. That financial push-and-pull is still clouding — and in some cases distorting — many households’ views of an otherwise sunny economy, while leaving others more hopeful.

‘I can’t run on the hamster wheel fast enough’

Meg Thomann, a communications director for a pharmaceutical company, is one of Jim LaPointe’s customers. She and her husband, an architect, are renovating the historic home they share with their three kids. While they have the disposable income to do so, Thomann said it still “feels like I can’t run on the hamster wheel fast enough.”

In the middle of fixing her roof and preparing to add a new deck, her homeowners insurance provider dropped her $3,000 a year policy. The new ones she found were at least triple that, which she suspects is because of her home’s age.

Thomann showed NBC News the quotes she had to choose from: “This one’s at $9,500. We got one at $10,500, and a whopping $12,800.”

Insurers have been hitting many homeowners with steep hikes since the pandemic, with some backing out of risky markets altogether. Insurance rates jumped 32% from 2019 to 2023, largely because of big storm payouts and inflation, according to the Insurance Information Institute.

While stubborn inflation has raised doubts about when the Fed might start cutting rates, many homeowners remain locked into low-rate mortgages in a market with fewer homes for sale than usual. For contractors like LaPointe, that has meant a steady stream of repairs and upgrades among those unable or unwilling to move. “They can’t go anywhere,” he said.

In the meantime, consumer spending is cooling but hardly collapsing. Retail sales came in flat for April after an unexpected jump in March. While executives at some big brands say consumers are finally tightening their belts, others see the reverse — with shifting shopping habits positioning them to prosper.

If you look at purchasing power, it is actually increasing.

Kayla Bruun, senior economist, Morning Consult

Many households, particularly low-income ones, are trimming their overall spending as credit card balances and delinquency rates balloon. But other consumers are cutting back in one area so they can keep shelling out in another.

In nearly every major U.S. city, restaurants have seen surging weekend and evening traffic more than compensate for lunchtime declines, the payment processor Square said this month. Airlines and cruise operators are bracing for another summer of record travel demand, including for high-end packages.

“If you look at purchasing power, it is actually increasing,” said Kayla Bruun, senior economist for Morning Consult. Average weekly wages are up around $200 since 2019 and are now rising faster than overall inflation — as they’ve done for roughly the past year.

‘Everything will work out’

The widespread pay and hiring gains of recent years have cooled off lately, but some job seekers remain confident nonetheless.

Recommended

“I feel like everything will work out,” said Alexia Godinez-Thompson, 22, who graduated this spring with a communications degree from Howard University in Washington, D.C.

The class of 2024 is entering a still strong but slowing job market where demand for their diplomas has sagged. Employers are comparatively hungrier for part-time and service-sector roles that don’t require higher education, and the tech and media industries have been hit with painful layoffs this year.

Me personally, my single self cannot change how the economy’s going.

Alexia Godinez-Thompson, Howard University class of 2024

Godinez-Thompson started college in the depths of the pandemic, experiencing her first two semesters through a computer screen at her mom’s house in Raleigh, North Carolina. After that shaky start, she said, “I just feel like I’m not equipped to go into the workforce,” but added, “I don’t feel the need to stress that much over it.”

She’s already secured an arts internship with Bloomberg Philanthropies this summer, paying $24 an hour. And despite having only a few hundred dollars apiece in her checking and savings accounts, her longer-term job search is already bearing fruit, boosting her hopes.

“Me personally, my single self cannot change how the economy’s going,” she said. “I can only be here, right now.”

‘You kind of start out behind’

Many Americans are less Zen.

Consumer sentiment took a sharp dip this month after bounding higher around the start of the year. With inflation stuck in the mid-3% range, people “really feel the sting of having to pay more than they remember paying a few years ago,” Bruun said. Consumers are more likely to internalize these frustrations than celebrate any benefits from higher pay, stock gains or home equity, she added.

Shaquille Washington is a mother of two in Jackson, Mississippi, earning a little over $9 an hour cleaning hotel rooms. She loves being able to work while her young kids are in school and finishes in time to pick them up. But money is a constant struggle.

Earlier this month, as the Dow Jones Industrial Average topped 40,000, she remarked that she doesn’t buy stocks, she buys groceries.

“The wages go up,” she said, but “the cost of living goes up times five.”

Prices in Jackson haven’t surged that high in reality, but inflation in the Southern region that includes Mississippi were 3.9% higher in April than the year before, hotter than the 3.4% rate nationwide. And Washington is paid less than the $12.41 hourly “poverty wage” threshold MIT researchers calculate for a single adult raising two children in the city — for whom a “living wage” would be $39.48.

Across the income spectrum, families have been blindsided by the costs of child care, which surpassed those of in-state college tuition in half the country, NetCredit researchers found last year.

I don’t think anybody our age is thinking when they’re in their early 20s, ‘I have a couple of years before I have to save for day care.’

Sarah Montoure, Cambridge, Wis.

In Cambridge, Wisconsin, nurse anesthetist Sarah Montoure and her husband, Kevin, who’s also a nurse, were facing the prospect of spending $665 a week on day care for their toddler son and infant daughter. With that expense threatening to gobble up one of their paychecks, they recently decided Kevin would begin staying home to care for the kids.

“It’s been, I guess, just shocking and at times disappointing to me that we can work really hard and start a family, and then you kind of start out behind,” said Montoure, 33. “I don’t think anybody our age is thinking when they’re in their early 20s, ‘I have a couple of years before I have to save for day care.’”

‘Retirement can be a reality’

Christina Cantu-McKay, however, gives her personal economy an A+ grade.

The 47-year-old law professor in Arizona spent more than two decades struggling with $100,000 in law school loans, making minimum payments that barely dented her balance as interest piled up. Then the Biden administration canceled it, to Cantu-McKay’s relief.

“I am starting to feel it now with my finances,” she said, with what used to be her student loan payments going into her 401(k). “Retirement can be a reality, and that’s pretty amazing.”

“It looks like I fit in the middle class now,” she said.

No comments:

Post a Comment